RBI का बड़ा तोहफा Small NBFCs को! 1 जुलाई 2026 से Registration और Reserve Fund की ज़रूरत खत्म — आपके Loan और NBFC Investments पर क्या पड़ेगा असर?

RBI has exempted small NBFCs with assets below ₹1,000 crore — that don't use public funds and have no customer interface — from mandatory registration and reserve fund requirements, effective July 1, 2026. Tagged as "Unregistered Type I NBFCs," these entities can also apply for deregistration by December 31, 2026 via RBI's PRAVAAH portal — India's first structured exit route from NBFC regulatory framework!

RBI का NBFC Amendment 2026 — छोटे NBFCs के लिए नई आज़ादी

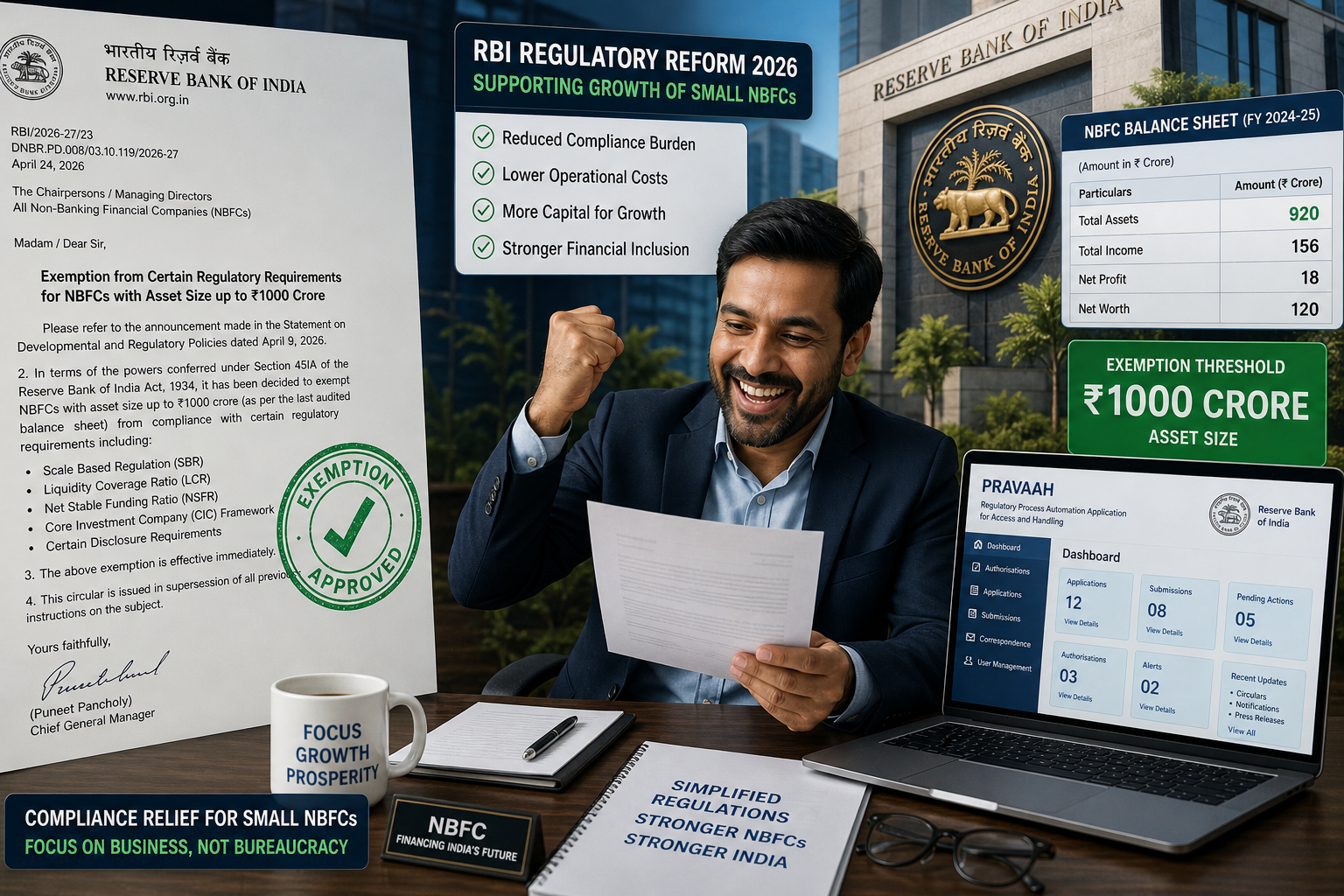

29 अप्रैल 2026 को Reserve Bank of India ने एक ऐसा circular जारी किया जो India के Non-Banking Financial Companies (NBFC) sector को fundamentally reshape करेगा। हज़ारों छोटे NBFCs जो अब तक mandatory registration, compliance burden और reserve fund requirements से जूझ रहे थे — उनके लिए एक बड़ी राहत आई है।

यह सिर्फ एक regulatory tweak नहीं है — यह India के NBFC ecosystem में proportionate regulation की एक historic shift है।

नया नियम क्या है? — Simple भाषा में

RBI ने final guidelines जारी की हैं जिसके तहत वे NBFCs जो तीन conditions पूरी करती हों — उन्हें registration और reserve fund की ज़रूरत नहीं होगी:

Condition 1: ₹1,000 करोड़ से कम की asset size (latest audited balance sheet के अनुसार)

Condition 2: कोई public funds नहीं — यानी न deposits, न bonds, न debentures लोगों से

Condition 3: कोई customer interface नहीं — यानी general public के साथ कोई direct lending या financial dealings नहीं

Effective Date: 1 जुलाई 2026 से।

"Unregistered Type I NBFC" — नई Category का मतलब क्या है?

RBI ने इन छोटे, low-risk NBFCs को एक नया tag दिया है — "Unregistered Type I NBFC।"

यह entities:

RBI के साथ mandatory registration से exempt हैं

Section 45IA (registration requirement) से free हैं

Section 45IC (reserve fund — net profit का 20% हर साल transfer) से free हैं

लेकिन RBI Act के relevant provisions के तहत अभी भी governed रहेंगी

RBI को direction देने या action लेने का अधिकार reserved है

तीन NBFC Categories अब:

🟢 Unregistered Type I NBFC

Public Funds/Customer Interface: नहीं

Asset Size: ₹1,000 करोड़ से कम

Registration: ज़रूरत नहीं

🟡 Registered Type I NBFC

Public Funds/Customer Interface: नहीं

Asset Size: ₹1,000 करोड़ से ज़्यादा

Registration: ज़रूरी

🔴 Type II NBFC

Public Funds/Customer Interface: हाँ

Asset Size: कोई भी

Registration: ज़रूरी

India का पहला Structured Exit Route — Deregistration कैसे होगा?

यह इस amendment का सबसे historic पहलू है। पहली बार RBI ने NBFC regulatory framework से structured exit route बनाया है।

Existing NBFCs जो Unregistered Type I criteria पूरी करती हैं — वे 31 दिसंबर 2026 तक deregistration के लिए apply कर सकती हैं।

Application कहाँ करें: RBI का PRAVAAH portal

ज़रूरी Documents:

पिछले 3 साल की audited financial statements

Statutory Auditor का certificate — जो confirm करे कि कोई public funds नहीं, कोई customer interface नहीं

Board Resolution — यह commitment कि future में भी यही conditions बनी रहेंगी

Physical surrender of Certificate of Registration (CoR) भी RBI के पास जमा करना होगा

RBI का अधिकार: अगर RBI को लगे कि business model genuinely और durably Type I नहीं है — तो वह deregistration refuse कर सकता है।

"Regulatory Arbitrage" रोकने के लिए Tight Definitions

RBI ने एक important safeguard add किया है — indirect public funds को भी public funds माना जाएगा।

मतलब — अगर कोई NBFC खुद तो public funds नहीं लेती, लेकिन उसकी group company funds लेकर उसे pass करती है — तो भी वह public funds में count होगा।

यह provision इसलिए critical है क्योंकि बड़े business groups अपनी investment holding companies को इस exemption का फायदा उठाने से रोका जा सके।

Auditors को मिला नया और बड़ा Role

इस framework में Auditors की ज़िम्मेदारी significantly बढ़ी है:

अगर कोई Unregistered Type I NBFC public funds या customer interface की conditions violate करे — तो Auditor को directly RBI को exception report file करना होगा।

यह एक major shift है — Auditors अब सिर्फ company के लिए नहीं, RBI के watchdog के रूप में भी काम करेंगे।

Family Offices को मिली Structuring Flexibility

इस amendment का एक underrated benefit है India के Family Offices के लिए।

अब तक family offices को अपनी investment activities private trusts, AIFs या RBI-registered NBFCs के ज़रिए structure करनी पड़ती थीं। नए framework में — जो investment vehicles public funds नहीं लेतीं और customers से deal नहीं करतीं — वे RBI registration के बिना corporate structure में operate कर सकती हैं।

यह India को global proportionate regulation practices के करीब लाता है।

Reserve Fund Rule से छुट — ₹ करोड़ों की Savings

अब तक हर registered NBFC को Section 45IC के तहत अपने net profit का 20% हर साल एक reserve fund में transfer करना पड़ता था।

छोटी NBFCs के लिए यह एक बड़ा cash flow burden था। Unregistered Type I NBFCs को अब यह करने की ज़रूरत नहीं — यह capital वे growth, operations या returns में use कर सकती हैं।

आपके Loan और NBFC Investments पर क्या असर?

अगर आप NBFC से Loan लेते हैं:

यह exemption सिर्फ उन NBFCs पर apply होती है जिनका आम public के साथ कोई dealing नहीं। जो NBFC आपको loan देती है — वह Type II category में आती है और उस पर सभी RBI regulations पहले की तरह लागू रहेंगी। आपके loan, EMI और rights पर कोई असर नहीं।

अगर आप NBFC में invest करते हैं:

Unregistered Type I NBFCs public funds नहीं लेतीं — इसलिए आप इनमें directly invest नहीं कर सकते। ये purely internal capital से चलती हैं।

IFSC और Banking Connections:

GIFT City के कई investment vehicles इस new framework का फायदा उठा सकते हैं — जिससे IFSC ecosystem में और flexibility आएगी।

Expert View — क्या है असली मतलब?

यह amendment दो तरफा है:

Positive Side:

Genuine low-risk NBFCs के लिए compliance burden कम होगा

Ease of doing business बेहतर होगा

Resources regulation पर नहीं, business growth पर लगेंगे

Concern:

Complex business groups technically compliant रहते हुए financial activity को RBI supervision से बाहर रख सकते हैं। Smart structuring और layered funding के through regulatory gaps का use हो सकता है। लेकिन RBI ने group-level fund flows track करने के लिए indirect public funds definition को tight रखा है।

निष्कर्ष — India के NBFC Sector का Maturity Moment

RBI का यह NBFC Amendment 2026 एक well-calibrated policy decision है। यह उन low-risk, internal investment entities को unnecessary compliance burden से मुक्त करता है जो कभी public funds लेती ही नहीं थीं। साथ ही customer-facing NBFCs पर — जो आपको loans देती हैं, जो आपके savings को mobilise करती हैं — सभी protections पहले की तरह intact हैं।

अगर आप IFSC-linked banking services use करते हैं, NBFC से loan लेते हैं या fintech apps के ज़रिए credit access करते हैं — आपके अधिकार और protection में कोई बदलाव नहीं आया है। यह reform India के financial system को globally competitive, proportionately regulated और more business-friendly बनाने की दिशा में एक ज़रूरी कदम है।